Why ETH will win store of value

For years, I viewed Bitcoin as the most asymmetric risk-reward of our lifetimes. It had unique properties that made it the best store of value the world has ever seen. And difficult-to-replicate network effects made it unlikely that another cryptocurrency would displace it.

Through September 2020, Bitcoin was the only cryptocurrency I owned. The store of value TAM was so huge, it made little sense to allocate capital toward anything else. The broad market for storing value could be as high as $400 trillion, and it struck me as extremely likely that Bitcoin would capture a significant percentage of the "monetary premium" from the following:

- gold ($10T)

- bonds ($100T)

- equities ($30T)

- real estate ($200T)

- broad money ($100T)

- art, wine, collectibles ($20T)

What could possibly compete with that kind of upside? Besides, most other cryptocurrencies were scams, and the few legit projects didn't seem to have yet found product-market-fit.

Then, at the prodding of a friend, I reluctantly started buying some Ether. Smart contracts and decentralized applications were cool, don't get me wrong. But in my mind it was foregone conclusion that Bitcoin was going to win the value store use case, and that was the ultimate prize. I also was unsure of how value would accrue to Ethereum's native asset.

A few months ago this view started to change. As almost anybody in the crypto space can attest, once you own a little bit of something, you pay a lot more attention to it. And two developments caught my attention: 1) Ethereum's migration to proof-of-stake and 2) changes to the protocol's monetary policy. I soon realized that these changes—-among others—-would have massive ramifications for ETH's monetary properties that might even make it a superior store of value to BTC.

Naturally, I was skeptical at first. After all, Bitcoin already has such a massive head start. It's a household name, it's the most secure in terms of hash power, and massive institutions such as Tesla, MicroStrategy, and MassMutual have already started adopting it as a reserve asset. Could Ethereum really catch up?

But the more I read and thought about it, the higher the probability I assigned to the world converging on Ether as a store of value. I soon converted most of my BTC to ETH and decided to write this essay to clarify my thoughts.

In my view, Ethereum will win the store of value war for four main reasons:

- More Scarce

- More Secure

- Organic Demand

- Real Yield

I realize such a suggestion will likely come across as blasphemous to the Bitcoin maxis out there. I side with these maximalists on a lot of fronts, such as the need for a pristine asset that allows people to preserve their wealth over time. However, I'm less dogmatic on how we get there. I'll ultimately back whichever asset I think gives us the best shot. And to borrow from Paul Tudor Jones, Ethereum looks like the fastest horse right now.

More Scarce

Stores of Value

In my previous essay, "Why Bitcoin Makes Sense," I wrote extensively on what makes for a good store of value so I won't spend too much time on definitions here (see the section "What is money and why are some forms of money better than others?" for a quick primer).

The basic premise is that money is simply technology that makes our wealth today available for consumption tomorrow. Thus the "best" money is the one that will give its holder the most purchasing power over time. There are several factors that influence a monetary good's suitability as a store of value, but the most important is supply growth or scarcity.

Have you ever wondered why gold emerged as the predominant store of value throughout human history? Why not silver or copper or one of the other 118 elements? The primary reason is scarcity. The growth rate of gold's supply has historically hovered around 2%. Only silver comes close with an annual growth rate of 5-10%, rising to around 20% today. An extremely low supply growth rate allowed gold to maintain its purchasing power over time better than anything else, and the world eventually converged on it is a store of value.

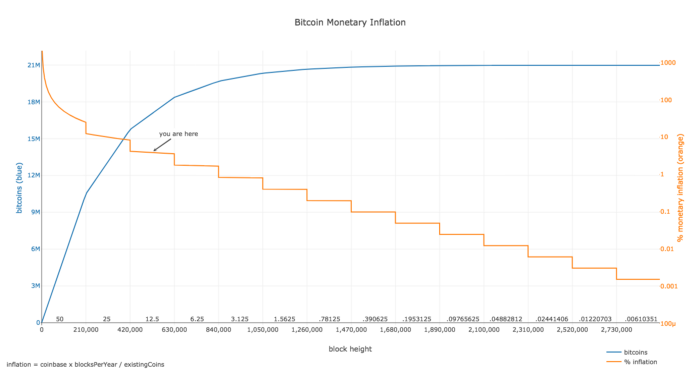

For thousands of years, gold was the best we could do in terms of a limited-supply monetary good that could maintain its value over time. However the invention of Bitcoin created the first truly scarce form of money to ever exist. With Bitcoin, we have a precise measurement of supply, 21 million bitcoins, that anyone can audit with their home computer. Bitcoin took what gold did better than anything else, and improved on it by an order of magnitude. Yet, Ethereum might just do the same to Bitcoin with the migration to proof-of-stake and an upcoming change to its gas management.

Ethereum's Monetary Policy and EIP-1559

Ethereum's current yearly network issuance (i.e. inflation rate) is around 4.5% with 2 Ether per block and an additional 1.75 Ether per uncle block (plus fees) rewarded to miners. Ethereum does not have a fixed supply because a fixed supply would also require a fixed security budget for the network. Rather than arbitrarily fix Ethereum's security, Ethereum's monetary policy is best described as "minimum issuance to secure the network."

Bitcoiners hate this ambiguity because they believe that the base layer of the financial system should be stable. Bitcoin’s development is intentionally careful and slow, and no more than 21 million bitcoins will ever exist.

The Ethereum community believes that they are sacrificing this near-term stability for long-term network security, and the fact of the matter is that Ethereum does have a history of reducing issuance to these estimated minimums. Furthermore, the move to proof-of-stake (PoS) will allow for a drastic reduction of Ether issuance while maintaining the same level of network security. I'll expand more on this later, but Vitalik has a great essay on his blog explaining how proof-of-stake is able to offer more security for the same cost.

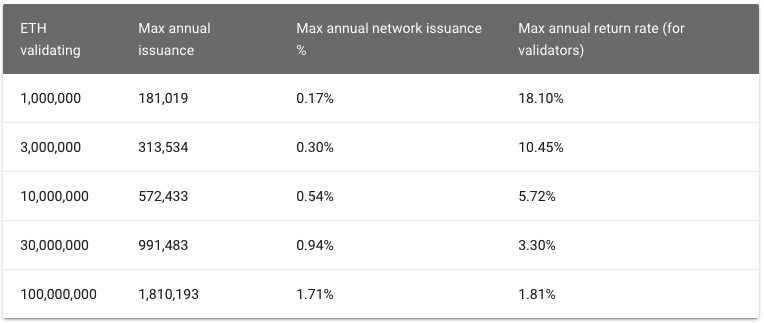

According to the current Eth 2.0 spec, Ethereum's issuance rate will be greatly reduced as part of PoS. Instead of new issuance going to miners, it will go to validators who stake their ETH to process transactions and agree on the state of the network (more details here). And there will be a sliding scale between total amount of Ether at stake and annual interest earned by stakers. The current spec would produce the following annual interest and inflation numbers based on total network stake:

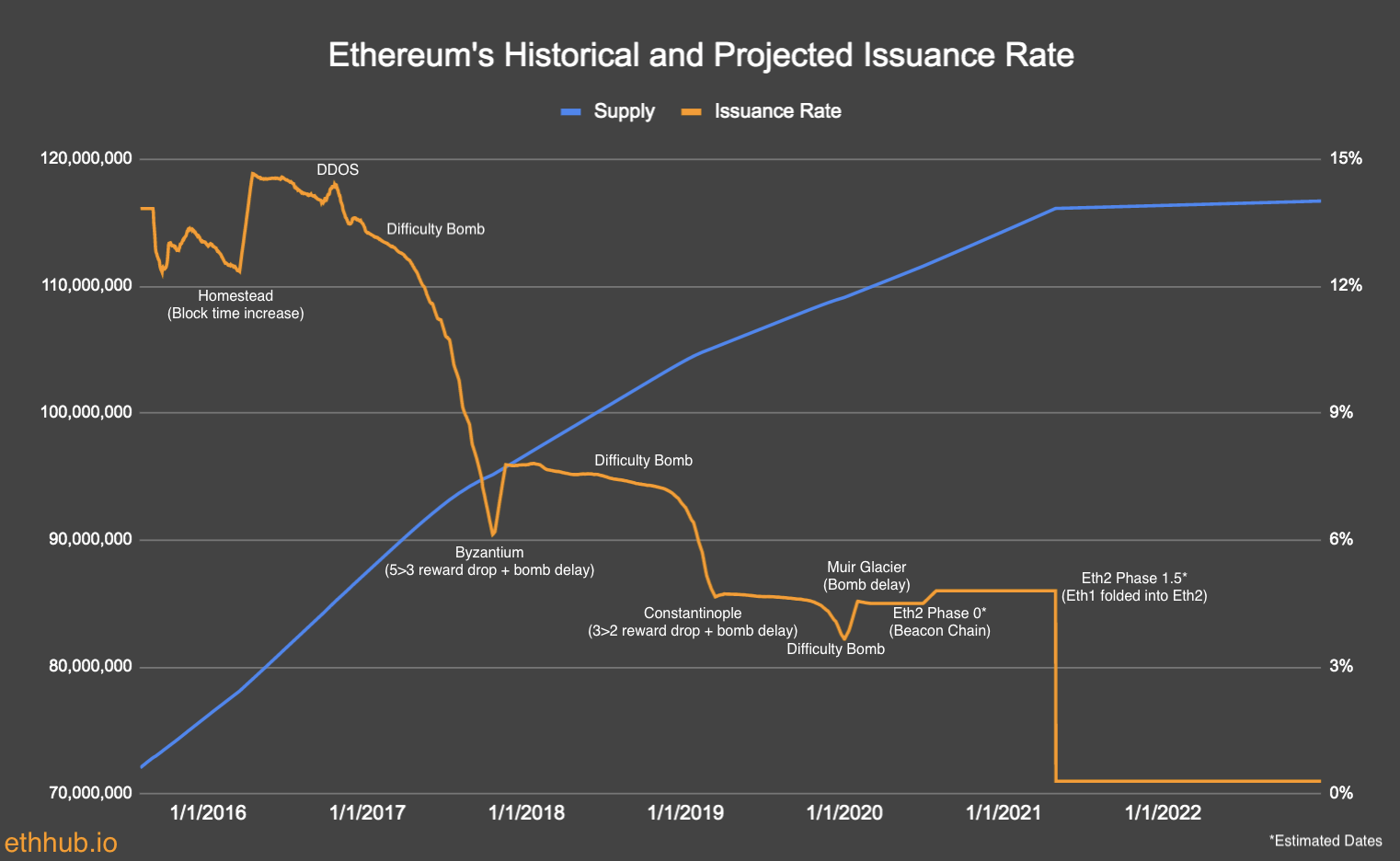

Basically, we can probably expect annual network issuance (i.e. inflation rate) to fall from ~4.5% today to less than 1% after the transition to PoS. The chart below highlights this massive drop well:

But that's still more than Bitcoin, which has a capped supply of 21 million BTC and a long-run inflation rate of 0%. So how exactly is Ethereum more scarce? Well, there's more. Ethereum has begun to address many of the concerns around its monetary policy with the upcoming release of Ethereum Improvement Proposal (EIP) 1559, which has been called "Ethereum's scarcity engine" or "ETH's burn mechanism".

EIP-1559 is set for release in July as part of Ethereum’s upcoming London hard fork. Diving into the details of the proposal is beyond the scope of this essay, but the key aspect to pay attention to is that in addition to improving ETH gas UX, EIP-1559 will burn a portion of ETH transaction fees. This will permanently remove a portion of supply from circulation and decrease the daily net issuance of ETH.

Last year, an analysis of network transactions showed that EIP-1559 would have burned nearly 1 million Ether in 365 days, which is equivalent to almost 1% of the entire network. And as demand for Ethereum transactions grows, many expect this number to increase over time. Thus, when combined with the lower issuance required for PoS (less than 1%), Ethereum will actually have a deflationary monetary policy.

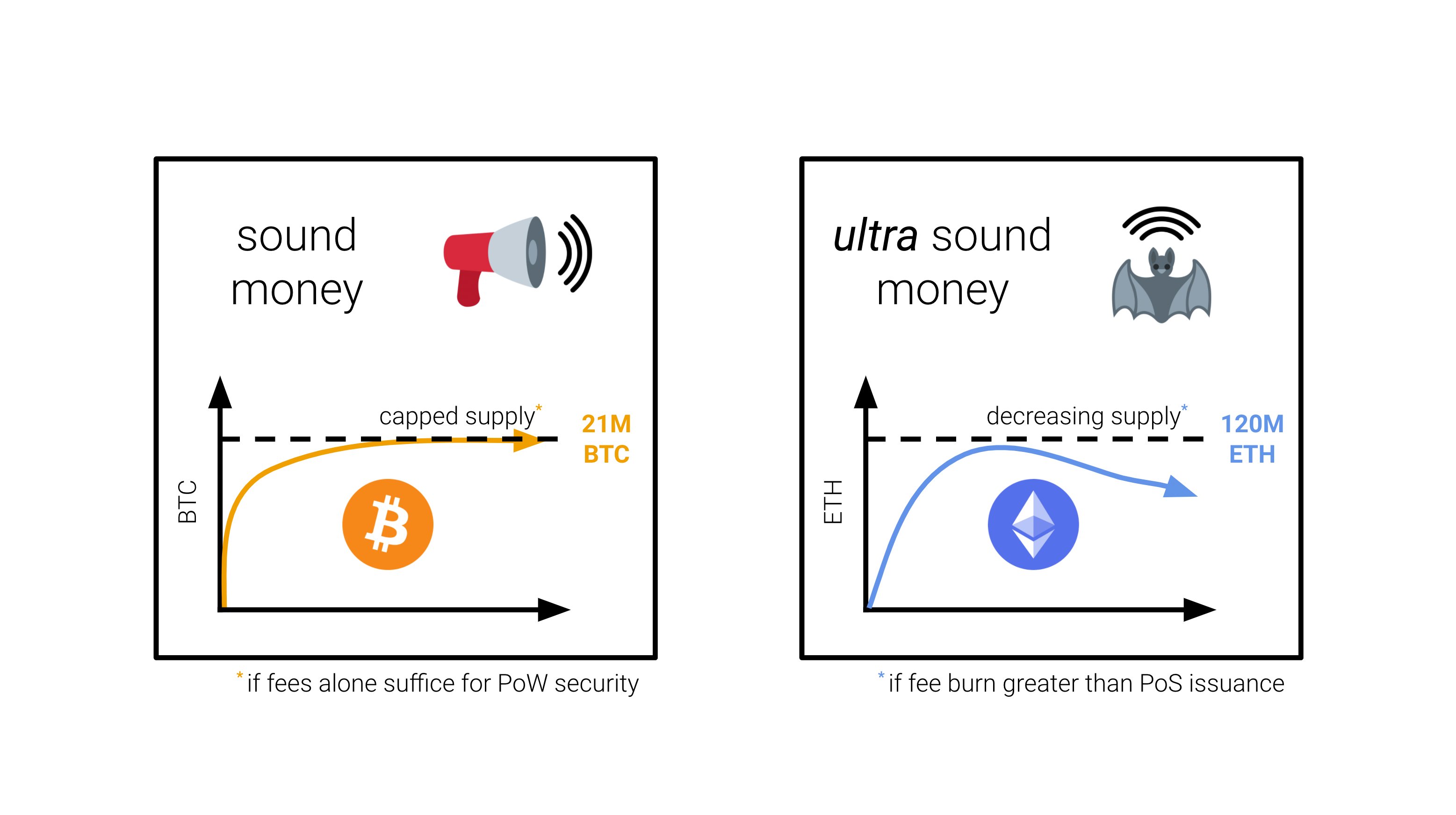

This has recently led to the new meme in the Ethereum community of "ultrasound money", coined by Ethereum researcher Justin Drake. The term is a little silly, but the point that Drake makes is that if Bitcoin is "sound money" because its supply is capped at 21 million, then a cryptocurrency with decreasing aggregate supply should be superior, hence the term "ultrasound money."

In the long run, Ethereum will be the more scarce asset. However, I'm probably even more bullish shorter term. With the removal of proof-of-work, ETH’s issuance will drop by around 90%. This is estimated to have the equivalent impact on miner selling pressure as three Bitcoin "halvings".

Stock-to-Flow and the Migration to Proof-of-Stake

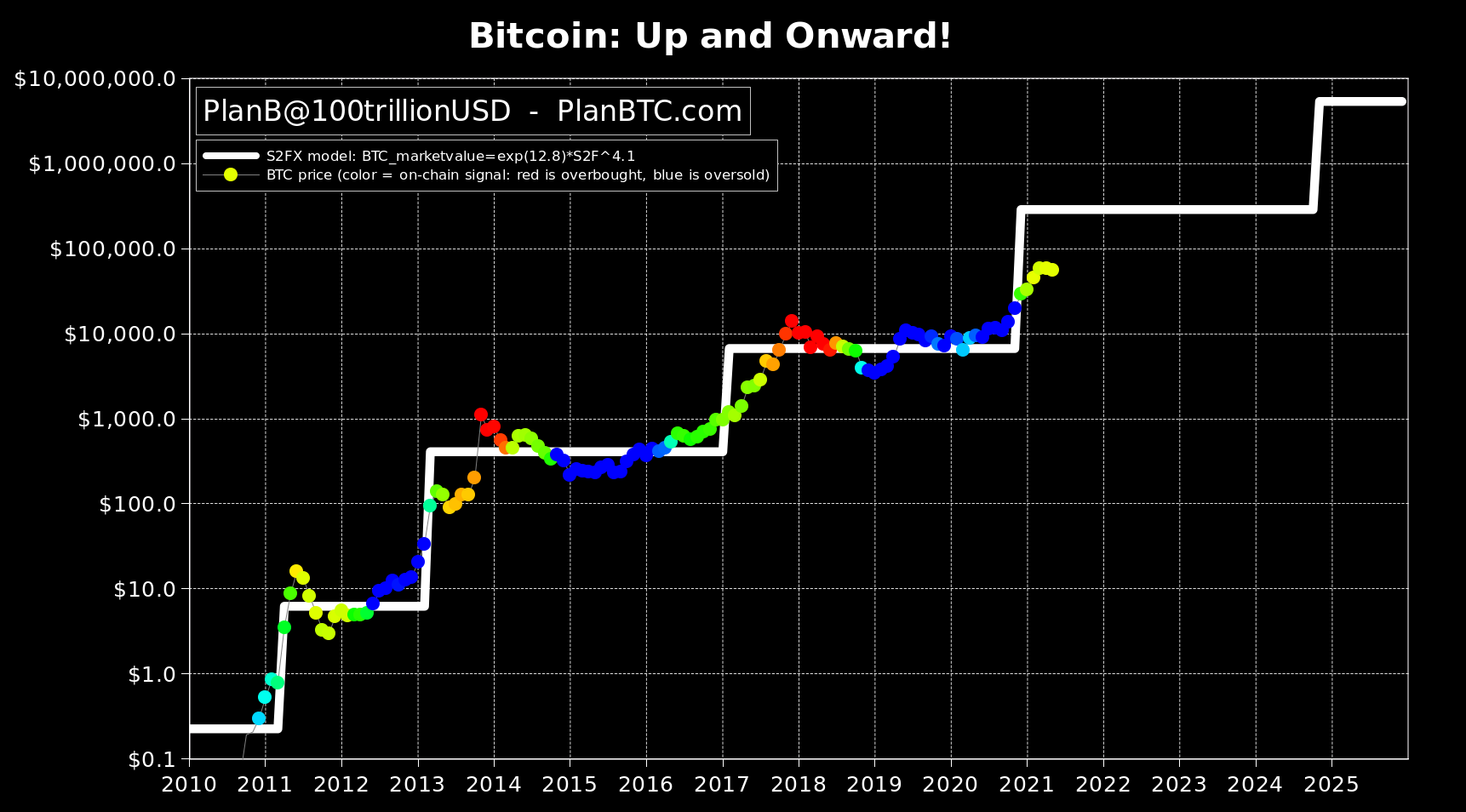

The best attempt at quantifying Bitcoin's scarcity and using it to model Bitcoin's value comes from PlanB's stock-to-flow model. He essentially argues that scarcity—-defined as the rate of supply growth—-directly drives value. The more scarce an asset is (lower supply growth rate), the more valuable it is. Below is a chart he created to help make his point ("SF" stands for "stock-to-flow" and is simply the inverse of the supply growth rate):

The shocking part is that this model has held up extremely well in the two years since he published it. In the chart below, the white line is the forecast, and the multi-colored dots represent the price of Bitcoin through May 2021.

As we can see, there are large jumps in Bitcoin's modeled value every four years. This is because the block reward paid out to Bitcoin miners is cut in half every 210,000 blocks (roughly every 4 years). And because block rewards are the only way new bitcoins can be minted, Bitcoin's supply growth is cut in half every four years.

As PlanB articulates (and quantifies) in his essay, this drop in supply growth is highly correlated with surges in Bitcoin's price. This is likely because it directly cuts selling pressure from miners in half. Because Bitcoin uses the resource-intensive proof-of-work (PoW) consensus mechanism, miners must sell bitcoins to cover their hardware and electricity costs. So when the block reward was halved from 12.5 bitcoins per block to 6.25 in May 2020, selling pressure from miners fell from 1,800 bitcoins per day to 900. This equated to a difference of roughly 1.6% of Bitcoin's market cap (almost $18 billion at today's prices) that isn't being sold every year by miners. With such a large supply shock, it's only natural we'd see the price of BTC skyrocket until it reached a new equilibrium level at the reduced inflation rate.

Ethereum, currently uses the PoW consensus mechanism today as well. But when it fully transitions to PoS, the ~4.5% annual Ether issuance will drop to less than 1%. This will equate to more than 3.5% of Ethereum's market cap (more than $15 billion at today's prices) that isn't being sold every year by miners. Further, I'd expect even less selling pressure because the block rewards will be distributed to stakers who are not forced to sell because hardware and electricity costs are minimal. To be fair though, most stakers will have to sell some ETH to pay income taxes on their reward, so new market supply won't go to zero.

Of course there are many other drivers of an asset's value than just scarcity. Acceptability by others is another. However, scarcity-—at least for now—-appears to be the most important factor in a good's monetary value because it leads to salability across time. On the other hand, security is also crucial factor. Just as gold is immune to rot, corrosion, and other types of deterioration, a cryptocurrency must be built to last through proper incentive engineering. After all, an asset that's not around in a few decades wouldn't be much of a value store.

More Secure

With gold, you get security free. The laws of physics handle everything from no forgeability to no double spend. With cryptocurrencies, however, you have to continually pay to keep the network secure.

With Bitcoin, specifically, a new block is created every 10 minutes. This block contains newly minted bitcoins (the "block subsidy") plus transaction fees, which together comprise the "block reward". Per Bitcoin's hard-coded monetary policy, the amount of newly minted coins per block decreases over time, eventually reaching 0% in the year 2140. When this happens and there is no new BTC issuance, the sole compensation for miners will be transaction fees.

Many Bitcoiners don't believe this will be an issue because the dollar value of transaction fees will be so high when the block reward runs out that security spend will be sufficient. In his essay "Bitcoin's Security is Fine", Dan Held writes:

"I hypothesize several hundred billion, in present value USD, would be an adequate security budget since it would be very difficult for a government to justify such a waste of an expense to just 51% attack the tip of the Bitcoin blockchain. They would also have to respond publicly for such an attack as their citizens (taxpayers), businesses, and banks will all be invested in Bitcoin."

He then goes on to tackle a bunch of concerns people often raise with respect to solely relying on transaction fees for network security. I agree with many of Held's arguments and understand why Satoshi designed Bitcoin this way. With proof-of-work, there is always a tradeoff between inflation (block subsidy) and security. Bitcoin has made the specific tradeoff where it will keep paying its consensus engine less and less so that it can maintain scarcity and cap the number of Bitcoins that will ever exist at 21 million.

However, I disagree that the USD-denominated security spend is what matters and side with what Vitalik Buterin wrote, in a recent reddit post:

"the security needs of a thing have to be proportional to the size of that thing, because as a thing gets bigger, its enemies become bigger and more well-motivated. If BTC were 100x as big as it is today, the value from destroying it would be 100x higher, and the kinds of actors that would want to care about destroying it would be much bigger and scarier. This is also why countries of all sizes have roughly similarly sized militaries as a percentage of GDP. Hence, cost of attack divided by market cap really is the correct statistic to measure, and in the long run issuance-free PoW really does look not that good."

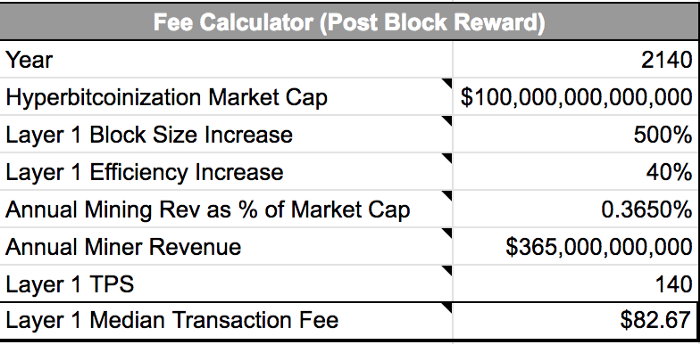

So let's look at Held's most optimistic scenario where Bitcoin "survives, thrives, and continues to grow in market share exponentially, as it has done the last 10 years". In this scenario, Bitcoin has a $100 trillion market cap in the year 2140 and transactional demand for Bitcoin's block space results in $365 billion of annual miner revenue (i.e. security spend).

Is $365 billion enough security spend to protect the Bitcoin network against attackers? Maybe. I'm really not sure and have no idea what the world will look like in 2140. However I'm pretty sure we can do better. The above scenario for Bitcoin's proof-of-work consensus mechanism would result in a value-to-security ratio of about 273-to-1. With Ethereum's proof-of-stake consensus mechanism, we can get to a value-to-security ratio of about 10-to-1. At the same market cap as Held projects for Bitcoin, this would equate to a roughly $10 trillion cost to 51% attack the Ethereum network (more than 27x better than the $365 billion Held projects for Bitcoin). And the only thing this really assumes is that roughly 10% of all ETH is staked, which seems pretty reasonable. Meanwhile, Held's projection assumes a 500% increase in block size and a 40% increase in efficiency, as well as significant transactional demand for Bitcoin's block space.

In addition to a much lower value-to-security ratio, Ethereum also has a major advantage in terms of how it can respond to an attack. After a 51% attack, the Bitcoin network's only option is to move from Double SHA-256 ASICs to a new proof-of-work system. This new system would have to be based on commodity hardware, such as GPUs or CPUs, because there wouldn't be enough time to manufacture the hardware for another ASIC proof-of-work system. The attacker would then have to just do the same 51% attack with commodity hardware. Vitalik has called this a "spawn camping attack", where a 51% miner cartel keeps attacking over and over again, rendering the chain useless. With a proof-of-work system, there is no way to destroy the mining power (or otherwise penalize) an attacker.

Ethereum (and proof-of-stake more broadly) are less susceptible to this kind of attack. This is because the Ethereum network can "slash" or penalize attackers. If an attacker does something bad, the network will penalize the attacker by seizing their staked ETH. This would be the Bitcoin equivalent of destroying an attacker's mining equipment, which obviously is something that can't be done by the protocol.

Ethereum actually has two types of slashing mechanisms. The first one, which can be called "layer one" slashing, is triggered if you do something clearly wrong within the protocol itself (e.g. two conflicting attestations), in which case the Ethereum network will automatically slash at least one third of your ETH stake. This deals with most potential attacks and redistributes ETH from dishonest nodes to honest nodes, making the system antifrigile in a way. The system gets stronger each time it gets attacked if you look at it through the lens of what's referred to as an "iterated game" in game theory. So let's say the attacker wants to attack again. He would have to go out, acquire even more ETH, do the attack again, and then get slashed again. With each attack, the amount of ETH in circulation is reduced and you can actually put a cap on the number of times the system can be attacked. Let's say, for example, that there's 100 million ETH outstanding and 10% of that is being staked. For each attack, the attacker would have to buy at least 10 million ETH, and every time they get slashed, they would have to go out and reacquire another 10 million ETH. In the worst case scenario, an attacker could only attack the system nine times. Furthermore, each attack will get increasingly costly as the price of ETH on the open market would likely rise with the the drop in supply.

Similarly, this antifragility also exists at the single-game level. If you want to attack the Ethereum network, you must acquire 10 million ETH (using the simplified numbers from above). And due to simple supply-demand dynamics, the more Ether you want to buy, the more expensive it will be as ETH available for sale decreases, resulting in diseconomies of scale (e.g. the second 1% of ETH supply you acquire, will cost more than the first because there's less ETH available for sale after you first bought 1% of all ETH outstanding).

A common argument that gets made to assuage fears of a miner or pool getting 51% hashpower is: even if they do, why would they attack? That would destroy the golden goose that lays their eggs; it's not in their interests. But in reality, we cannot assume this; not only does it assume rationality, it assumes lack of outside incentives. The whole point of having high levels of security is to protect against attackers with outside incentives to break the chain. This is why Vitalik's approach to thinking about PoS security is "if they have $X billion, how many times can they break the chain before all their money gets slashed?". It's not about assuming rationality; it's only assuming limits on bad actors' economic resources.

Perhaps the best argument I have heard in favor of proof-of-work's security is that the physical hardware-driven nature of it adds friction to even very well-capitalized attackers: you need to wait a year for the hardware to get manufactured, the process necessarily involves many people, and there's a high risk that it gets detected while you're doing it. This is a genuine advantage of PoW. That said, there is also a crucial downside to physical hardware: it's very hard to mine at significant scale without being detected, whereas PoS is much more censorship-resistant.

The lack of footprint required to stake Ethereum is a huge advantage when it comes to security. To become an Ethereum validator, all you really need is Ether, a raspberry pi, an SSD, and an internet connection. This is in stark contrast to Bitcoin where being a miner requires a massive footprint in the form of tremendous energy usage and huge warehouses to house the mining equipment. This footprint makes it relatively easy for governments to detect and shut down mining activity. Whereas with Ethereum, you could be anywhere in the world (perhaps behind a Tor network so you don't even have to leak your IP address). And even if a nation state were able to find and confiscate the physical Ethereum validating equipment, that's not where the staked ETH exists. Ether exists solely in the digital world and can only be confiscated by somehow getting the owner to hand over their private keys.

People sometimes forget that when Satoshi Nakamoto created Bitcoin over a decade ago, it was the world's first successful attempt at creating digital scarcity and incentive engineering for a proof-of-work consensus system. While clearly brilliant, the person or group operating under the Nakamoto pseudonym was in fact human and could not reasonably be expected to anticipate all of the potential issues that arise with incentive engineering. Since then there has been more than 12 years of research and development in the blockchain space working on network security and scalability. Bitcoin's issuance schedule was heavily influenced by that of gold because that was the best that the physical world could provide. But, for reasons detailed above, the design space increased dramatically when money moved to the digital world.

In my view, it seems like a pretty good bet that Ethereum will be the more secure network in the long run.

Organic Demand

In 1944, the Bretton Woods Agreement laid the foundation for the United States to obtain a near-global lock on the international monetary system. However, after only a decade, the Bretton Woods system began to fray. The US started running large fiscal deficits and experiencing mildly rising inflation levels, first for the late 1960s domestic programs, and then for the Vietnam war. Soon, the US began to see its gold reserves shrink as other countries started to doubt the backing of the dollar and redeem dollars for gold. This persistent reduction in gold reserves against growing external liabilities eventually forced Richard Nixon to end the convertibility of dollars to gold in 1971. However, the United States was still able to re-order the global monetary system with itself at the center. And we can learn from this as we try to predict which cryptocurrency will become the dominant global reserve asset.

After the breakdown of the Bretton Woods system, every currency was a fiat currency. This was the first time in human history that all currencies in the world were rendered into unbacked paper. There was nothing of value in the currencies themselves. They had value because governments declared them to have value and enforced their usage as a medium of exchange and unit of account by making all taxes payable only in that currency, or by enacting other laws to add friction to (or in some cases outright ban) other mediums of exchange and units of account.

However, outside of the United States, there was still little reason for foreign businesses and governments to accept pieces of paper, which could be printed endlessly and had no firm backing. But, as it turned out, the US was able to coerce universal adoption of the dollar by creating persistent international demand for it through the petrodollar system.

In 1974, the United States and Saudi Arabia reached an agreement. Saudi Arabia (and other countries in OPEC) would sell their oil exclusively in dollars in exchange for US protection and cooperation. Even if Germany wanted to buy oil from Saudi Arabia, for example, they did so in dollars. From then on, any country that wanted oil needed to be able to get dollars to pay for it. As a result, non oil-producing countries began selling many of their exports in dollars so that they could get the dollars they needed to buy oil from oil-producing countries. And all of these countries stored excess dollars as foreign-exchange reserves.

This system reinforced itself over time. As Lyn Alden wrote in her terrific article "The Fraying of the US Global Currency Reserve System" (where most of the above is borrowed from):

At first, countries needed dollars so that they could get oil. After decades of that, with so much international financing happening in dollars, now countries need dollars so they can service their dollar-denominated debts. So, the dollar is backed by both oil and dollar-denominated debts, and it’s a very strong self-reinforcing network effect. Importantly, most of those debts aren’t owed to the United States (despite being denominated in dollars), but rather are owed to other countries. For example, China makes many dollar-based loans to developing countries, as do Europe and Japan."

It is this "self-reinforcing network effect" that led everyone in the world to accept otherwise worthless pieces of paper issued by the US government for tangible goods and services. And it is absolutely fundamental to how the dollar became the global reserve asset of the world. Why does this matter? Well, I believe a similar system—-and virtuous cycle—-is developing around the Ethereum network.

For the last decade, the demand side of most crypto-networks has been dominated by speculation. There is nothing wrong with that. Speculation has provided the funding to pay for building out the supply side of these networks (infrastructure, applications, etc.). But this is now changing. You need ETH to do things on the Ethereum network. And people are doing things on it. They're buying domains, trading tokens, lending and borrowing, issuing bonds, using prediction markets, making payments, buying insurance, buying art, gaming, buying land in the metaverse, racing horses, and more. All of these require ETH to pay transaction fees and use them.

As the applications built on top of Ethereum get more complex and intuitive for users over time, demand for Ether will grow. 94 of the top 100 crypto projects are built on Ethereum, and more than 3,000 dapps and 200,000 ERC-20 tokens live on top of it. Total transactions on Ethereum are reaching new all-time highs every day, and the average value transacted on Ethereum is more than double that of Bitcoin.

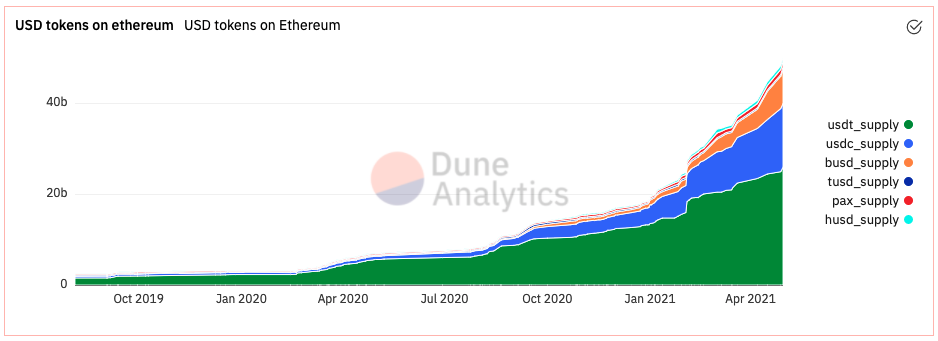

Some of the numbers are truly astounding. More than $80 billion of ETH is locked in DeFi, up from $16 billion in January. Decentralized exchanges, such as Uniswap and Sushiswap, are now accounting for a total of $432 billion of trading volume on Ethereum in the last 12 months as these automated market makers have made swapping tokens easier than ever before. And total stablecoin supply on Ethereum has increased from $19.5 billion in January to more than $48 billion today.

Ethereum is emerging to not only be the settlement layer for nearly all of the leading decentralized applications, but also for almost the entire ecosystem of digitized dollars. Even traditional financial service companies such as Visa will allow for transaction settlement to occur with USDC on Ethereum, displaying how stablecoins are now moving well beyond traditional crypto use cases. And just a couple weeks ago, the lending arm of the European Union, used Ethereum to issue €100 million ($121 million) in two-year digital notes for the first time.

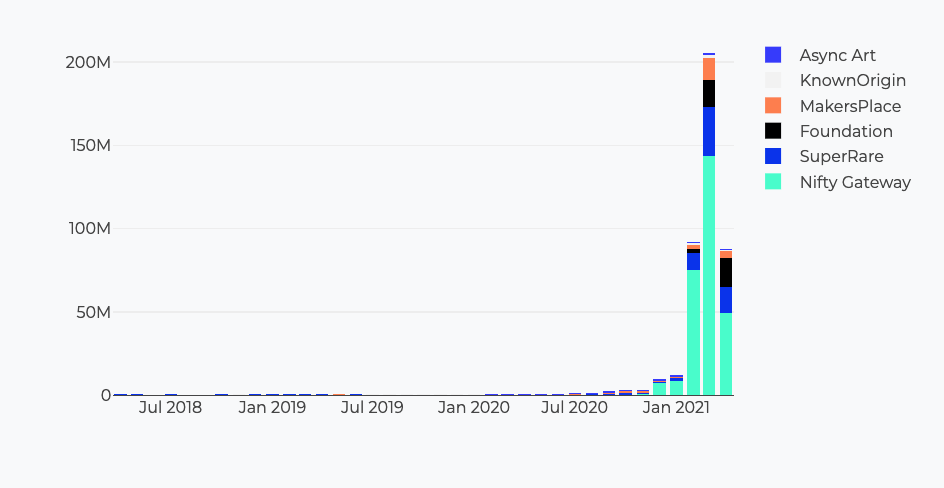

Furthermore, sales of NFTs (Non-Fungible Tokens) on Ethereum have surpassed $600 million, with 13 pieces selling for more than $1 million each. The use cases, are simply exploding.

Again, if you want to interact with the Ethereum network for any of the above-mentioned use cases, you have to pay a fee to the miners/validators who process your transactions. Ethereum is essentially a decentralized computer, and the compute power costs money. The fees are called "gas", and the resemblance to oil is uncanny.

The more useful applications built on Ethereum become, the more demand there will be for Ether. The TAM for DeFi alone—-using collective banking revenue as a proxy-—has been estimated to be $2.7 trillion (2%-3% of global GDP) per year. Knowing this, it becomes easy to see how a petrodollar-like system might develop around the Ethereum network. Let's just take Lyn Alden's quote above and change a few words:

At first, everyone needed Ether so that they could use the world's decentralized computer. After decades of that, with so much international financing happening in Ether, now countries need Ether so they can service their Ether-denominated debts. So, Ether is backed by both demand for compute and Ether-denominated debts, and it’s a very strong self-reinforcing network effect.

It might seem far-fetched to compare the demand for the Ether to the demand for oil, but if the world's financial infrastructure lives on Ethereum, is it actually? It seems increasingly likely to me that Ether will benefit similarly from this self-reinforcing network effect that made the dollar the world's global reserve currency.

Overall, Ethereum imitated Bitcoin in many ways but offered a substantial improvement by creating a virtual decentralized computer that greatly expands the potential use cases. And these use cases provide organic, sustainable, and growing demand for Ethereum block space. As these use cases flourish and become more widely adopted, demand will only grow larger. And simply using basic supply-and-demand economic principles, it's reasonable to expect Ethereum's price (and thus purchasing power) to rise faster than Bitcoin's in the long run. It is more scarce, and the decentralized computer aspect shifts the demand curve dramatically.

Because the "best" money is the one that will give its holder the most purchasing power over time, this organic demand further improves Ethereum's odds of winning the store of value war.

Real Yield

George Soros will probably go down as the greatest currency trader of all time. And in his book, The Alchemy of Finance, he reveals much about his decision-making process. Chapter three is titled "Reflexivity in the Currency Market" and describes both vicious and benign circles in currency markets. In it, Soros argues that there are a number of mutually self-reinforcing factors in traditional currency markets that create cycles characterized by wide fluctuations in exchange rates, interest rates, inflation, and/or economic activity levels. The chapter gets pretty technical but let's just focus on his points on the key drivers of speculative capital: rising exchange rates and rising interest rates.

We focus on speculative capital because it is one of the three main drivers of exchange rate movements, along with trade and non-speculative capital flows (i.e. "fundamentals"). In reality, "fundamentals" (which we covered in the previous "More Scarce" and "Organic Demand" sections) are also influenced by market participants' expectations about the future course of exchange rates. This is just one example of Soros's idea of "reflexivity", and it's pretty easy to see it in Ethereum where speculation has driven many investors and developers to invest both their time and money building out the network infrastructure and applications on top of it. Speculative capital is in fact essential to the fundamentals. And both have a mutually self-reinforcing relationship where more speculative capital generally leads to stronger fundamentals, which in turn drives even more investment and so on. And as Soros describes, rising exchange rates and rising interest rates are the primary drivers of speculative capital:

"Speculative capital moves in search of the highest total return. Total return has three elements: the interest rate differential, the exchange rate differential, and the capital appreciation in local currency. Since the third element varies from case to case we can propose the following general rule: speculative capital is attracted by rising exchange rates and rising interest rates. Of the two, exchange rates are by far the most important. It does not take much of a decline in the currency to render the total return negative. By the same token, when an appreciating currency also offers an interest rate advantage, the total return exceeds anything that a holder of financial assets could expect in the normal course of events."

So let's break that down a bit. Exchange rates are by far the most important. This makes sense. If I earn 8.5% interest staking ETH but the price falls by 10%, I lose money. So we really shouldn't focus on interest rates until we can be sure that the exchange rates will rise. This is why most altcoins with 1,000%+ APYs are awful bets and Bitcoin was such a great bet for the last 12 years. It's also why I focused on the key factors that will drive the price of Ether higher in the first three sections of this essay. Assuming those assumptions are correct, we can now turn our attention to interest rates which could enter into a mutually self-reinforcing relationship with the price and eventually help drive the world to converge on Ether as a store of value.

Let's assume that Bitcoin and Ethereum have equally-compelling monetary properties and the market expects the price of both assets to appreciate at 100% this year. In this scenario, a rational investor shouldn't have a strong preference for either asset. However, if you give that same investor the ability to earn 6% staking their Ether on Coinbase or 8%+ if they run a validator themselves, things start to change. While a 100% expected return might not seem so different from a 106% return, in the long run it makes all the difference. This is especially true as the expected asset appreciation falls from 100% to more reasonable levels as cryptocurrencies become less speculative and the market becomes more efficient. Over time, 6% will likely comprise an ever-increasing portion of Ether's expected total return.

The extra 6%+ risk-free yield you can earn staking ETH, will incentivize some investors to shift funds from Bitcoin to Ethereum. This is just how markets work. For example, since 2008, the U.S. has experienced ~$8.5 trillion of inflows from foreign investors, the bulk of which began picking up in 2011 as investors searched for higher returns in the form of carry (higher bond yields in the U.S. relative to zero- or negative-yielding bonds in Europe and Japan). Speculative capital naturally flows toward assets with the highest expected real yields.

What will be a benign circle for Ethereum will be a vicious circle for Bitcoin. As more and more speculative capital flows from Bitcoin to Ethereum in search of higher real yields, expectations for exchange rates between the two currencies will also change. This won't happen overnight, but with time I anticipate that market expectations for Ethereum price appreciation will be higher than that of Bitcoin. And when that happens, that things could get ugly for Bitcoin. As Soros writes:

"The longer a benign circle lasts, the more attractive it is to hold financial assets in the appreciating currency and the more important the exchange rate becomes in calculating total return. Those who are inclined to fight the trend are progressively eliminated and in the end only trend followers survive as active participants. As speculation gains in importance, other factors lose their influence. There is nothing to guide speculators but the market itself, and the market is dominated by trend followers. These considerations explain how the dollar could continue to appreciate in the face of an ever-rising trade deficit."

I love Bitcoin and everything that it stands for, but this scenario is looking more and more likely with each passing day. And I wonder what will happen when Ethereum's market cap surpasses that of Bitcoin for a sustained period of time. If Bitcoin isn't the most liquid asset in crypto, what is it?

Another aspect to consider that I won't spend too much time on is that staking and yield farming on DeFi suffice for passive day-to-day income for most of the large ETH holders. They no longer need—nor want—to sell ETH when they can passively earn 8%+ just staking and even higher rates yield farming. This should further bolster Ethereum's scarcity and expected price appreciation going forward.

Risks & Concerns

In summary, these four factors are the primary reasons I believe Ethereum will ultimately win the store of value war. Of course, the conclusions I draw above are far from certain and this essay would not be complete without at least touching on many of the risks to this thesis. Because this essay is already super long, I'll briefly comment on each one.

Scaling Challenges

At the present moment, transaction speed suffers when the network is busy which can make the user experience poor for certain types of dapps. And as the network gets busier, gas prices increase as transaction senders aim to outbid each other. This can make using Ethereum very expensive. A couple of months ago, gas prices to complete a simple transaction were as high as $100-$200, though they did drop with the Berlin upgrade, which coincided with new Ethereum price all-time highs.

This is probably the most crucial risk to Ethereum, as it has opened the door of opportunity for competing projects, such as Solana which is doing some interesting stuff in the space. Ultimately, Ethereum has many options at its disposal to improve the network's speed, efficiency, and scalability. The layer 2 solutions and sharding are probably the most notable. But they are not without technical risks though, and they're needed urgently.

Other Layer 1 Solutions

Part of me can't help but wonder if Ethereum will eventually be displaced by a cryptocurrency that learns from Ethereum's trials and improves upon it in some fundamental way. There are many "Eth-killers" out there attempting to capitalize on Ethereum's foibles and become the top dog—-including Polkadot, Solana, Cosmos, Cardano, etc.

As Peter Thiel explained in one of his Stanford startup lectures, "People often talk about 'first mover advantage.' But focusing on that may be problematic; you might move first then fade away. More important than being the first mover is the last mover. You have to be durable."

Two years before Amazon, there was Book Stacks Unlimited. Four years before Google, Yahoo! made the original global search engine. Before Facebook, MySpace dominated social media. The list goes on. There are countless examples throughout tech history of first movers generating interest in a concept or product, and then late movers swooping in and improving upon what already exists.

But Ethereum has strong protections against this risk of obsolescence. It has many of the same network effects that Bitcoin has, and the Ethereum community and protocol is innovation-friendly, which might be just as important. "Bitcoin will absorb all innovation" was a meme that never came true. Ethereum actually has a shot at it, to a large extent because they have "feature escape velocity" at the EVM level.

I do acknowledge though that new developments in the space and risks must be adapted to on a continuous basis. But Ethereum looks like the best bet at the moment.

Monetary Policy Stability

Bitcoin is the most unchangeable crypto-system that will likely ever exist. Bitcoiners believe this is where the real value of Bitcoin lies. It's a credibly neutral system based on code, not people, that you can depend on for decades.

Ethereum's human-managed hard forks and centralized dev teams come with risks. How can we trust that Ethereum’s monetary policy won’t change again? How can we be sure that it won’t be a detrimental change? Even if the Ethereum community agrees it will never change, and it honors that, it will perpetually be 12 years behind the trust that has been built with Bitcoin.

This is an important concern if Ethereum is going to become the global value store, but as argued above, I believe Ethereum is sacrificing near-term stability for long-term security. It is already very decentralized, and its centralized aspects have allowed them to innovate on security, monetary policy, and usefulness.

Increased Complexity

As is almost always the case in engineering, there are trade-offs moving from PoW to PoS. The first one is complexity. The Bitcoin proof-of-work system is beautifully simple and you could write pseudo code for it in a dozen lines of code. Unfortunately, Ethereum's proof-of-stake is orders of magnitude more complex. The state transition mechanism for the Beacon chain could be written in roughly 1,000 lines of code, so using that as a very rough proxy, we're looking at about a 100x increase in complexity. This is a real trade off—complexity leaves room for bugs and can create scaling issues among other problems. The good news though is that Ethereum has already paid for the cost of this complexity by proving that it is possible to overcome this complexity with four production-grade implementations securing the Beacon chain right now.

Fair Launch

Some people argue that Bitcoin has a "monopoly on fairness" because it was launched at a time when nobody knew what it might become. They argue that this is something that can no longer be replicated and gives Bitcoin some of its best properties. And anything that has a "pre-sale" cannot be considered fair. Further, Bitcoin's proof-of-work system is a terrific forcing function for distribution as miners must sell bitcoins to cover their hardware and electricity costs. Proof-of-stake does not have this property. Ethereum stakers will simply accrue more ETH and are not forced to sell because proof-of-stake is so efficient that hardware and electricity costs are minimal. Bitcoiners have argued that proof-of-stake installs a permanent plutocracy. However, as mentioned earlier, this is a bit of a misconception since income tax (~50% in many jurisdictions) will act as an economic forcing function. Furthermore, Ethereum has been on a proof-of-work system for almost six years and many Ethereum supporters argue that this has resulted in plenty of distribution. Also, do largely amoral market participants really care if the network is fair? I'd argue, most of them will just act in their own self interest and buy whatever asset they believe will make them the most money. Also who is to say what's a fair method of distribution and what isn't?

Objectivity

The last drawback I'll bring up is objectivity. When you run a full node on Bitcoin, you can sync all the way from the genesis block (first block ever mined) to today's latest transaction. With Ethereum, you can only sync up to the latest three months. So if you've been disconnected from the Ethereum network for more than three months, the only way to sync up is to ask a few semi-trusted sources what the current state is and accept it as an assumption. This is less than ideal because it is a compromise on trust, and most Bitcoiners will argue that it's unacceptable to not verify all of the transactions going all the way back to Genesis. However, in practice, the trust inherent in Bitcoin and Ethereum are roughly equivalent. As a Bitcoiner, when you download the client, you are trusting Bitcoin.org or whatever website you're using given that almost nobody will inspect the source code and read every single line of code. Bitcoiners also must trust bootstrap nodes. The very first time you connect to the peer-to-peer network, you connect to what are called "bootstrap nodes", which allow you to connect to the broader system. If for some reason your bootstrap nodes are compromised, you could be trapped in a fake system controlled by the attacker. So this objectivity argument is actually quite subjective.

Thanks to Justin Drake for inspiring many of the aforemantioned ideas and for reading the draft of this

Sources & Further Reading

- Bankless: Ultra Sound Money | Justin Drake

- A brain dump on PoS vs PoW arguments by Vitalik Buterin

- Why Proof of Stake (Nov 2020) by Vitalik Buterin

- Why Ethereum is Undervalued, featuring Ethereum co-founder Joe Lubin

- Yes... I Read the Whitepaper by Arthur Hayes

- EthHub: Monetary Policy

- Bitcoin vs Ethereum by Dan Held

- Bitcoin's Security is Fine by Dan Held

- The Fraying of the US Global Currency Reserve System by Lyn Alden

- Consensys: The Q1 2021 DeFi Report

- The Demand Side of a Crypto-Network by Fred Wilson

- The Alchemy of Finance by George Soros